In Canada, our economy is built by people who aren't afraid to get their hands dirty. From the long-haul truckers crossing the Rockies to the construction crews shaping our city skylines and the ride-share drivers keeping our communities moving—the hustle is real.

But for many, especially in the South Asian community where we often carry the weight of providing for extended family, there is one question we don't ask often enough: "What happens to my family if I can't work tomorrow?"

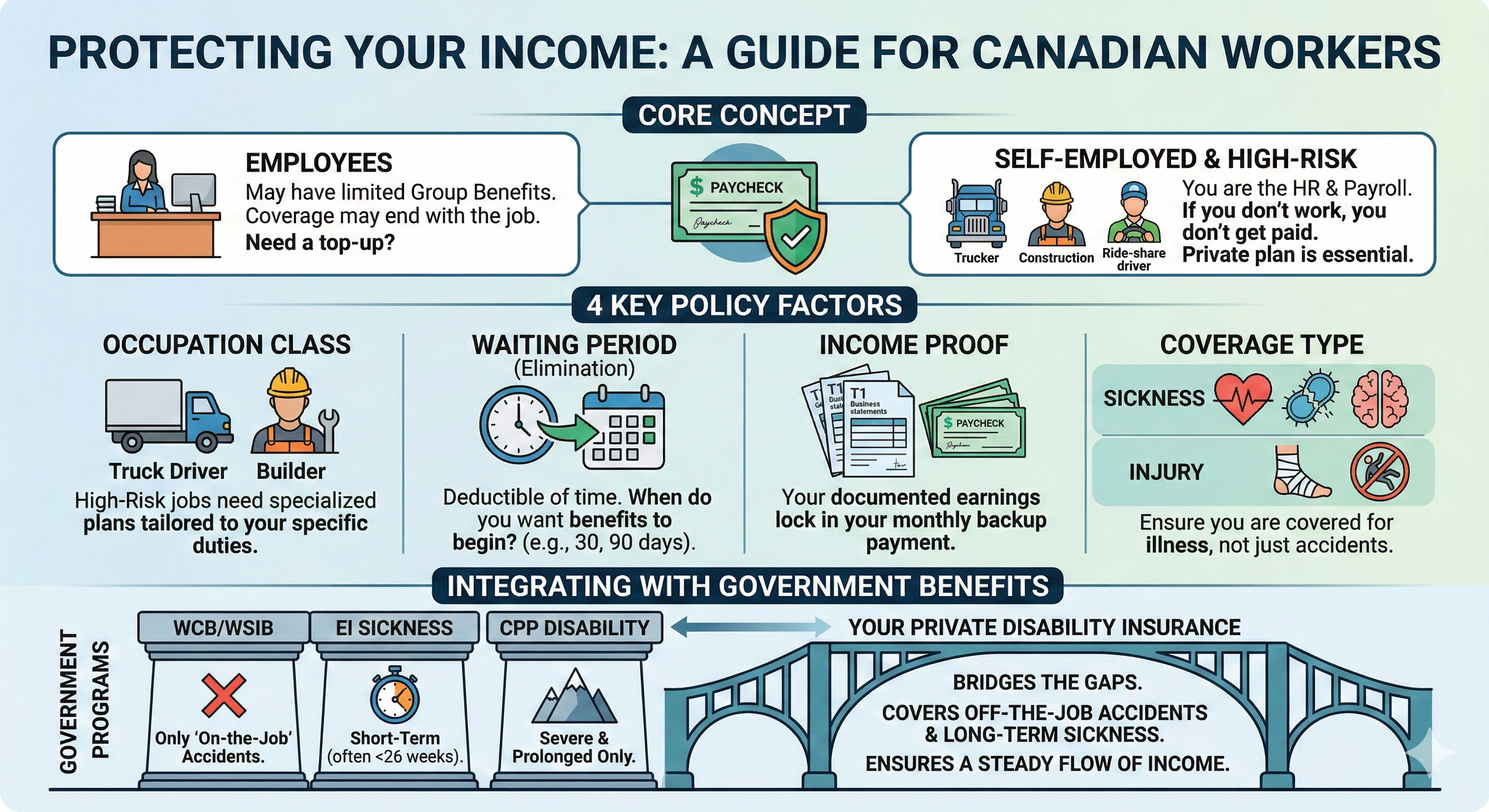

The Story of the Unseen Risk

Consider the story of Arjun, a dedicated owner-operator trucker. Arjun is the primary breadwinner for his wife, two children, and his parents. He is meticulous about maintaining his truck because "if the wheels aren't turning, I'm not earning."

One evening, while at home, Arjun tripped on a loose carpet and badly broke his wrist. It wasn't a "workplace accident," and it didn't involve his truck. However, he couldn't shift gears or secure a load for three months.

Because Arjun was self-employed, he had no "sick leave." His truck insurance covered the vehicle, but nothing covered him. This is where Disability Insurance (Income Replacement) becomes the most important tool in a worker's kit.

Why "Income Replacement" Matters for Everyone

Whether you are a salaried employee or a self-employed contractor, your lifestyle is funded by your ability to show up and work.

For Employees: Many people believe their workplace "Group Benefits" are enough. However, these plans often only cover a portion of your salary and disappear the moment you leave that company or if the business closes.

For the Self-Employed: You are your own safety net. If you don't work, the income stops, but the mortgage, truck payments, and grocery bills continue. Private disability insurance acts as a "backup paycheck" that you control.

Understanding the "Gears" of a Policy

When setting up a plan to protect your income, there are four main factors that determine how your coverage works:

Occupation Class: Insurance companies categorize jobs based on risk. A construction worker or a trucker has a different risk profile than an accountant. It is vital to have a policy that understands the specific physical demands of your job.

The Waiting Period: Think of this as a "time deductible." It is the number of days you must be unable to work before the insurance payments start (common periods are 30, 60, or 90 days).

Income Proof: For self-employed individuals, your benefit amount is usually based on your documented earnings (like your T1 General tax forms). Locking this in early ensures there are no surprises when you need to make a claim.

Age and Health: Like most things in life, it is easier and more affordable to set up protection when you are younger and healthy.

Sickness vs. Injury: The Full Picture

Many workers only think about "accidents"—falling off a ladder or a collision on the 401. However, statistics show that sickness (such as heart disease, cancer, or mental health struggles) causes significantly more long-term absences than physical injuries.

A robust policy should cover both. While "Injury-Only" plans are often easier to get without a medical exam, they leave you vulnerable if a sudden illness keeps you away from your job.

The Gap in Government Benefits

| Program | What it Covers | The Reality for Most |

|---|---|---|

| WCB / WSIB | Workplace injuries only. | If you get sick or hurt at home (like Arjun), it pays $0. |

| EI Sickness | Short-term illness. | Only lasts for up to 26 weeks and pays a maximum that is often much lower than a trucker's or contractor's actual bills. |

| CPP Disability | Severe and permanent. | Only pays if your disability is "severe and prolonged," meaning you likely can't work any job at all. |

Private Disability Insurance is designed to bridge these gaps. It provides a steady flow of income regardless of whether the injury happened at work or at home, and it can stay with you until you are ready to return to your specific career.

Final Thoughts

In our community, we take pride in our work ethic and our resilience. But true resilience isn't just about working hard; it’s about making sure that if life throws a curveball, your family’s future remains secure.

Understanding these benefits is the first step toward moving from "hoping for the best" to "planning for the future."